Image by Peter Selbach sourced from pixabay

The following is Part 2 in a two part series.

Part 1 of this series discussed my view of what volatility is and how it impacts investing. Here in Part 2, I present my read of the current volatility landscape and examine what it might mean for the general direction of investment markets. In short, I think it’s likely that we’ve entered, what I call, a “volatility deleveraging” period, characterized by de-risking.

What in the world is “volatility deleveraging”?

As we’ve already covered, volatility can be thought of as an expectation gap or confidence interval. While it is impossible to precisely know the current state of volatility in a given market, we all rely on some estimate of what it might be when making investment decisions. This process can be either implicit or explicit (most notably by utilizing measures of implied volatility).

The volatility environment, up until very recently, has been ahistorically benign. Whatever the underlying reason might be – central banks leaning on rates, quantitative easing (QE), subdued “inflation”, steady economic growth, short volatility trading strategies (like ETFs), geopolitical stability, what-have-you – the result has been low volatility. Making money in such an environment means sticking with what works, and what’s worked has been long duration, credit, equity, real estate, risk-parity, artwork, classic cars, … well, long almost anything, and especially passive instruments (which are really implicit momentum plays). Trading and rebalancing are a fool’s errand under such conditions.

As these strategies continued to work, money continued to feed them. It’s quite rational behavior, really. However, the longer such an environment persists, the greater the capital accumulation into stagnant strategies becomes. Investors lever themselves to the same world view, or at least to how much prices of various financial assets are expected to fluctuate. Up until recently, we simply did not believe that much change was possible in the markets – so said our positioning, not our mouths.

Well that might have all just changed.

It is important to note that nothing changes investors’ minds and mobilizes capital faster than losses, even if just of the paper variety. Losses indicate that predictions were wrong; the expectation gap closes via the price mechanism. The same holds true for gains (prices appreciate along with improving fortunes); however, the speed tends to be quicker in the case of the former. There’s an old trading adage that “markets take the stairs up and the elevator down.” Of course investors can be wrong for periods of time. “It’s tough to make predictions, especially about the future.”

The moves in the U.S. rates and equity markets have been swift and loss producing. This is a change, and change relates to volatility. If these changes are permanent, then capital must reallocate accordingly. I believe that the old regime has ended and that we have moved into one with greater volatility. If so, capital must de-lever from prior theses; hence volatility deleveraging. Remember, greater volatility typically results in less capital being risked, which should generally result in lower valuations.

How we might have got here …

Here’s how I see the volatility landscape potentially unfolding, beginning with my view of how we got here and why it might change. Continue reading at your own risk, as what follows is merely conjecture. It’s my best attempt at putting together the puzzle pieces within a volatility framework.

Lying at the heart of my thesis is the fictitious belief that the Fed and its peers saved the economy and bailed out the markets. To be sure, there is some fact in that statement. QE did directly recapitalize the banking industry and prop up the crumbling Eurodollar-based financial system that should have been left for dead. Granted, the latter scenario would have been extremely painful to endure and taken significant time and effort to remedy, but it was the proper play for long term prosperity … I digress.

In reality, QE – and to a lesser extent zero and negative interest rate policies (ZIRP and NIRP, respectively) – merely created widespread asset inflation, in my opinion (see here for more). Interest rates were driven to the lowest levels in recorded human history and volatility was suppressed. Were the central bankers solely responsible for this? It’s impossible to know for sure, but I’m skeptical of this view. History is littered with examples of markets laying waste to the best laid plans of central bankers (George Soros vs. the British Pound is a notable one), and as I’ve previously postulated, they are irrelevant in the long run.

However, I do find it plausible, if not likely, that QE exacerbated the impacts of how market participants were acting irrespective of monetary policy. Up until this day investors are feverishly buying “safe assets” – partially due to a lack of economic confidence, partially due to changes in banking regulations, partially due to the need to replace structured finance collateral in the Eurodollar financial system, and partially for lots of other reasons, I’m sure. It is my view that the central bankers created a “pile on” effect in bond markets by joining this popular trade, ultimately resulting in the widespread asset inflation seen today. This has occurred, in my opinion, because: 1) markets are integrated (meaning that what happens in one market can impact another), and; 2) the economic backdrop has been continuously improving; thus those who could move out the risk spectrum in search of higher returns have done just that (including my Grandma, true story).

It is important to realize that the central bankers did not trick anyone into believing things were better than they were (well, OK, perhaps they tricked some people, but not the market as a whole). The fact is that the economy has been healing from the financial crisis, albeit pathetically slow and, in my view, slower than it could have been.

Now of course investors are not dumb, and quite frankly, neither are central bankers. If central bankers were going to indiscriminately buy certain bonds – irrespective of price – investors would line up to take their money. “A fool and his money are soon parted.” Markets adapted. (Note, this is not to call central bankers fools, just that from an investment perspective it’s foolish behavior to be indifferent to price.) As long as QE remained a given fact and the economic backdrop remained stable, there was little questioning over the future direction of the investment markets: up and to the right. Investors felt comfortable taking risk. Everyone “knew” markets couldn’t go down (or only fall so far). The “Fed put” was in place. The evidence: QE 2, QE 3, the mimicking behavior of the European Central Bank and Bank of Japan, and every one of Bill Dudley’s comments following the first whiff of a stock market wobble. Those who “fought the Fed” lost, time and time again. Markets adapted.

The result: asset inflation and low volatility.

… why might it change …

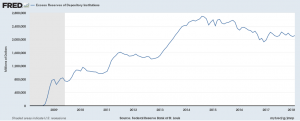

Given the above, I believe that interest rates lie at the epicenter of the volatility environment. Perhaps, being a fixed income guy, I’m biased. Though I think the narrative above makes a lot of sense, especially within the context of the financial crisis. QE played a part in recapitalizing the banking system and it used the bond market as a mechanism, in my opinion. Just look at all the excess reserves that were created, only to remain as such.

This begs the question: what, if anything, can be a catalyst for change? There are two related candidates at the top of my list: 1) the anticipated end of QE, and; 2) the possibility for investment losses.

Similar to the implementation of QE nearly a decade ago, investors will try to front-run the central bankers. They will seek to profit from the latter’s completely price-indifferent actions. While central bankers are unconcerned with price, they are quite concerned with how their actions will be judged by the public (I present you with Exhibit A). This is why, I believe, they obsessively try to communicate and over-communicate their intentions. They aspire to build a market consensus surrounding their actions in order to minimize the range of investors’ expectations. Said differently, they hope to narrow confidence intervals and suppress volatility.

Irrespective of all the #fedgibberish, markets will anticipate the coming end of QE. Not only does it, in my opinion, represent a material change to actual capital flows (and hence prices), but as importantly, introduces dissension among investors’ expectations for what lies ahead. Will the Fed actually follow through? If so, might they unwind faster or slower than initially communicated? Will other central banks follow suit, and if so, which ones and when? This diversity of opinion – which had been absent from discourse for years – ultimately means greater volatility.

Even if the “Fed and Friends” aim to move slowly, overwhelm us with #fedgibberish, and truly try to minimize their volatility impact, the damage may already have been done. Each upward tick in sovereign bond yields brings the duration risk, which had been mounting below the surface, to the fore. If losses mount, investors will mobilize their capital, reallocating it first from those segments of the capital markets most acutely affected, to those perceived as safest. A recent Bloomberg article chronicles the potential beginnings of such an occurrence in the investment grade corporate bond market.

The realization of losses seems almost surreal given the length of the current bull market. Of course, it’s healthy! Losses are a necessary part of investing for and creating a future world. However, investors have gotten accustomed to the “Fed put” having value. Yet here we are, the 10 year U.S. Treasury bond yield has risen by about 74 bps since the middle of September – shaving off nearly 2 years’ worth of coupon payments from the November series’ par value; the S&P 500 is approximately 9% below its all-time high; and there hasn’t been so much as a peep from the Eccles Building. It appears that the capital markets may be back to their properly functioning selves! However, for investors, this may mean that the “Fed put” has expired and that market declines are once again possible.

Remember: nothing changes investors’ minds and mobilizes capital faster than losses.

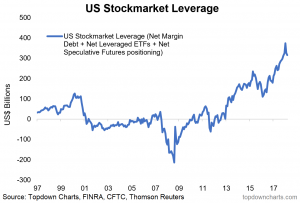

Are we at the beginning of a systematic deleveraging of volatility? Was the liquidation of the XIV ETF a discrete event, or part of a larger picture? The latter seems quite plausible to me.

… and what might that mean?

While I finger the potential end of QE and worthless expiration of the “Fed put” as important drivers of the recent market moves, there surely could be other factors at work (like the possibility for trade wars, “inflation”, etc.). Regardless, the process of rethinking the future direction of capital markets should lead to higher levels of volatility as confidence intervals surrounding expectations widen. I have certainly experienced this with my own thinking, and I doubt that I am unique. Also, losses incurred by strategies explicitly short volatility may temper their return, adding to the upwards pressure. Thus, we could very well see a regime change with respect to volatility.

A higher volatility environment should result in less capital being placed at risk, capital outflows, and lower prices. This will likely apply to “quants” and “fundamentalists” alike. The former’s models will mechanistically drive them to do so, as trailing measures of volatility feed in over time. Those acting more on trading instincts will de-risk when losses lead to tough conversations and actions. Risk management systems of all walks will likely reign in exposures, be it in the form of an investment committee, VaR model, risk department, delta hedge, gut feeling, broker, available margin, etc.

Need it all end in a Minsky Moment? I don’t think it must. Why couldn’t the volatility deleveraging occur over time, especially if economic conditions remain resilient? Minds typically change slowly and market tops form gradually, especially if no obvious problems, like a recession, are evident. And remember, it is we humans who program the bots. That said, panics do occur, if infrequent. Thus, I offer no opinion here.

It should be stating the obvious that I have no idea if this thesis is correct, no matter how good it sounds on paper. My views have been challenged by some really smart people, yet I still find myself coming back to them. I remain eagerly open to being wrong. Regardless from which angle I approach this topic – be it from a capital flow perspective, a thesis herding one, or through a volatility lens – I find the trail to end at the same conclusion: that the end of QE should be a negative headwind for investment markets … but only to the extent that it actually occurs.

The situation is fluid, to say the least. If, in the end, I am ultimately proven wrong (very possible, though not from lack of trying), volatility will be just fine, and it will be my bubble that bursts.