Knowing When To Walk Away, And When To Run

Source: pixabay

I’ve been suffering from a bout of writers block lately. I simply don’t have much to say with respect to how I’m thinking about the investment markets. This has been a little anxiety producing for me given that The Integrating Investor is still young and building an audience (many thanks to all of you for reading and helping to spread the word; readership is growing rapidly!). While my intention for creating the blog was predominantly self-serving – to journal my thoughts on investing in order to further develop and refine my own burgeoning framework – the more discussion and comments the blog generates, the smarter all of us participants should become. At least that’s the thesis.

As faithful readers know, my current working macro investment theme is tied to changes in the central bank liquidity landscape (see here and here for my earlier articles), and is irrespective of economic conditions (as a primary). Whether or not I am correct will be for history to decide. The recent uptick in volatility and selloff in various markets appeared to have (momentarily) validated this view. However, after some initial excitement, those asset classes that I intently watch – US corporate bonds professionally, and stocks, treasuries, and precious metals tangentially – have begun to progress in a sideways “chop”, which is neither confirming nor refuting of my thesis.

S&P 500 chart by TradingView

US 10yr Treasury yield chart by TradingView

Baa-rated corporate bond spreads by FRED

Gold price chart by TradingView

In fact, I’ve only recently come to appreciate that my thesis is, by its nature, a slow moving one. I’ve already vastly underestimated the length over which dramatic policy shifts occur, and by the looks of it now, the process could easily extend out over another year or two. This is a hard investment proposition for most professionals and amateurs alike. There is of course the alternative: that I’m just wrong. And the quicker I can realize this, the quicker I can move on to my next (hopefully profitable) thesis. Hence, I find myself bewildered, watching the markets, looking for clues.

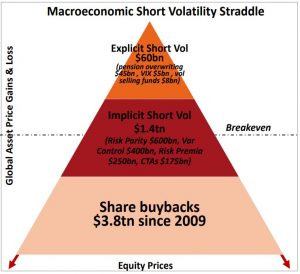

Specifically, I’m looking for signs of a volatility regime shift. I’m expecting the change in liquidity landscape (expected or real) to introduce more volatility into the investment markets and create one with higher averages, a bearish development. The mechanics of this view should be most easily observed with the stock market and the VIX. I suspect that some strategies that systematically shorted volatility may not return to their former strength after having likely incurred some recent losses. This reduction in sellers could reset the mean higher. Thus, any strategy that utilizes volatility as an input (risk-parity/smart-beta, volatility targeting funds, VAR-based risk management tools, etc.) could be forced to de-risk overtime as they adjust (see Chris Cole’s brilliant research on the topic here). Again, time will either confirm or refute this view.

Source: Artemis Capital, Volatility and the Alchemy of Risk

Periods of “fits and starts” have developed; bouts of activity sprinkled among periods of non-activity. This could be consistent with my view. Big changes in capital flows should logically create an increase in price volatility (as for why I believe this to be so will have to be the subject of another article). Volatility does not show up all at once and hang around; it comes and goes, and each of these regimes – the active and non-active – requires specific action.

CBOE VIX chart by TradingView

So as I sit here rubbing my eyes and scratching my head, I am reminded of a valuable lesson from the investing legends: the value of inaction. Sometimes it’s best to do nothing. Let your positions ride and wait. Below are some classic quotes about fighting the urge to be in the market when the proper course of action is ambiguous.

“The desire for constant action irrespective of underlying conditions is responsible for many losses on Wall Street even among the professionals, who feel that they must take home some money every day, as though they were working for regular wages.”

– Jesse Livermore

“There is a time for all things, but I didn’t know it. And that is precisely what beats so many men in Wall Street who are very far from being in the main sucker class. There is the plain fool, who does the wrong thing at all times everywhere, but there is the Wall Street fool, who thinks he must trade all the time. Not many can always have adequate reasons for buying and selling stocks daily – or sufficient knowledge to make his play an intelligent play.”

– Jesse Livermore

“Your job is to wait for the best opportunities. Money is made in stalking and sitting not being active and finding trades each day.”

– Dan Zanger

By no means am I suggesting that you follow course. There are plenty of ways to make money in any market. If you have some good ideas and are convicted, by all means take action, make money! The above are merely reminders that just because others are trading doesn’t mean that you have to, even if you’re a professional. Investments returns typically do not accrue linearly over time.

Remaining unconvinced of anything at the moment, I am reminded to sit tight, motivated by Warren Buffett’s words that “the price you pay determines your rate of return.” Though, I much prefer the wisest investment advice of all that I’ve come across:

“You got to know when to hold ’em

Know when to fold ’em

Know when to walk away

And know when to run …”– Kenny Rogers, The Gambler

Go ahead, hum along for a minute or two, no one’s judging. In fact, I’m going to take a little stroll and “walk away” myself in order to clear my head and fight the urge to trade while I wait to see what comes.

Charles hayes

I am impressed beyond all measures that you are Jesse Livermore fan. My reading of your review of the thinly veiled book about “ the greatest short seller ever” is a mark of your grounded view of the markets. Volitility and market moves are in reality the aggregate of billions of seemingly meaningless individual choices. I am a hard money guy when real cash is in be aware and longish, when the hard money begins falter or take a breather than like Jesse suggested or as Kenny sang take some cash off the table and begin to exit the stage with pockets full of cash.

Your articles are good, thoughtful and timely your information will gain a large following no worries there

Seth Levine

Thank you. Your readership and comment are greatly appreciated.